CIBIL (Credit Information Bureau India Limited) is a credit bureau in India that maintains the credit information of individuals and companies. It was established in 2000 and is licensed by the Reserve Bank of India (RBI) under the Credit Information Companies (Regulation) Act 2005.

CIBIL collects and maintains credit information from various sources, such as banks, financial institutions, and credit card companies, to create credit reports and credit scores for individuals and companies. These reports and scores are used by lenders to assess creditworthiness and make lending decisions. CIBIL plays an important role in the Indian financial system as it helps lenders manage credit risk and enables individuals to access credit products such as loans and credit cards.

CIBIL, now known as TransUnion CIBIL, is a credit rating agency that collects, maintains, and provides credit ratings for clients around the world. TransUnion CIBIL, which was founded in 2000, has 2,400 members, including financial institutions, NBFCs, banks, and home financing firms. As a credit agency, TransUnion CIBIL keeps credit histories for more than 550 million individuals and companies.

CIBIL Score is a three-digit number ranging from 300 to 900 that reflects an individual’s creditworthiness. It is based on the credit history of an individual and is used by lenders to determine the creditworthiness of an individual and evaluate the risk associated with lending money to him/her. A high CIBIL Score indicates that an individual is a low-risk borrower and is more likely to get approved for a loan or credit card. On the other hand, a low CIBIL Score implies that an individual is a high-risk borrower and is less likely to get approved for a loan or credit card.

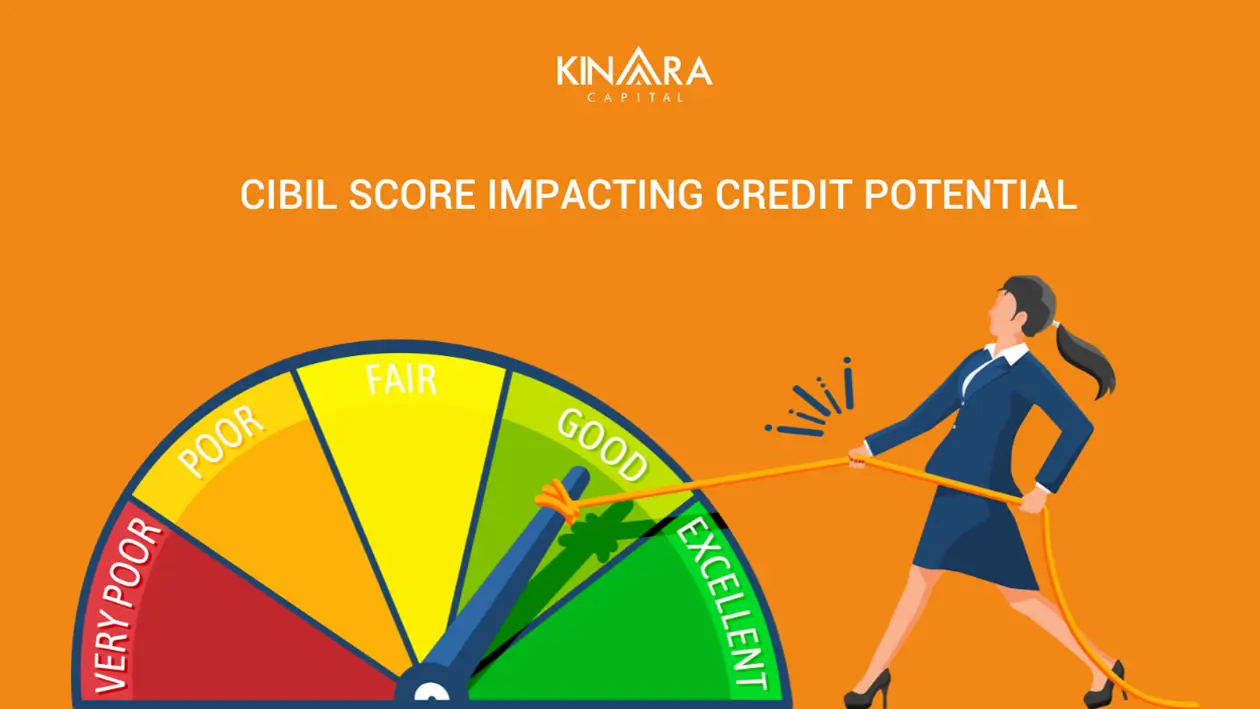

CIBIL score ranges from 300 to 900, and the score is divided into different ranges that represent an individual’s creditworthiness. The different CIBIL score ranges are as follows:

A score of 750 and above is considered excellent and indicates a very good credit profile. Individuals with a score in this range are more likely to get approved for credit products such as loans and credit cards and may also qualify for more favourable terms such as lower interest rates.

A score between 700 and 749 is considered good and indicates a healthy credit profile. Individuals with a score in this range are likely to get approved for credit products but may not qualify for the most favourable terms.

A score between 650 and 699 is considered fair and indicates a satisfactory credit profile. Individuals with a score in this range may face some challenges in getting approved for credit products and may also have to pay higher interest rates and fees.

A score between 550 and 649 is considered poor and indicates a weak credit profile. Individuals with a score in this range may find it difficult to get approved for credit products and may have to pay high-interest rates and fees.

A score below 550 is considered very poor and indicates a very weak credit profile. Individuals with a score in this range may find it extremely difficult to get approved for credit products and may have to pay very high-interest rates and fees, if at all.

CIBIL score shows NA/NH if an individual has no credit history, which denotes that either “not applicable” or “no history” applies. NA stands for Not Applicable and typically appears for individuals who have no credit history or have not used credit facilities in the past. In other words, if someone has never taken a loan or used a credit card, their credit report may show NA as their credit score. NH stands for “No History” and is similar to NA, indicating a lack of credit history. However, NH is typically shown for individuals who have not used credit facilities in the recent past or have not had any credit activity for a long time.

CIBIL Scores are calculated based on the information in an individual’s credit report. The credit report contains information such as the individual’s repayment history, credit utilisation ratio, types of credit used, and total credit limit. The score is calculated using a proprietary algorithm that considers all the information in the report. Factors such as timely payment of bills, low credit utilisation, and the mix of credit accounts all play a role in determining an individual’s CIBIL Score. Here are the factors that affect the CIBIL score:

Paying bills on time will increase a person’s credit score and help them drastically improve it. The CIBIL score is negatively impacted by missing payments or defaulting on EMIs. The determination of the CIBIL score is heavily impacted by the loan repayment history.

A person’s credit score is also influenced by the type of credit they have used; specifically, 10% of the CIBIL is affected by this. Using only one sort of credit will not improve the score. Completely refraining from using credit also has no positive effects. An individual needs to have a credit balance in order to generate a 10% positive contribution. Hence, borrowing both secured and unsecured loans is required. Another 15% of the CIBIL score is determined by the length of repayment. This is dependent upon how long a person has been utilising credit and whether or not he is consistently paying on-time payments.

The credit usage ratio is the proportion between the credit amount that is used and the credit amount that is available to an individual. If a person wants to have a healthy credit utilisation ratio, they should attempt to avoid using more than 30% of their available credit frequently. Even though having a CUR in the 60–70% range seldom has an impact on their credit score, a high CUR or regularly reaching the maximum of their credit limit suggests a stronger dependence on credit and a possibly large payback load, which may have a negative effect on their credit score.

Another aspect taken into account while determining a person’s credit score is credit inquiries. The lender will check their credit report each time when a person applies for a loan or credit card. This is referred to as a hard inquiry. Their credit score will suffer if they submit several credit requests in a short period of time. Hence, it is recommended to space out credit applications throughout the year rather than submitting them all at once.

CIBIL score can be checked online. Here is a step-by-step tutorial for determining CIBIL credit score:

Responsible credit behaviour is necessary for a high credit score. Also, it’s crucial to have a high CIBIL score because it influences whether or not banks will grant you a particular amount of credit. Your chances of receiving an easier credit approval increase with a high CIBIL score. Here are some elements that will assist you in keeping a high credit score:

Payment history accounts for almost 35% of the credit score computation. An individual’s track record of on-time repayment must be perfect if they want to always have an excellent credit score. They must take care to never skip a payment in order to achieve this.

The credit-seeking individual should keep their credit utilisation ratio around 30% of their total credit limit. This goal can be reached by distributing the cost of spending among a number of credit products. The individuals can improve and maintain their credit score, which will ultimately help them increase their level of financial security by reducing their credit utilisation ratio.

Lenders frequently make an effort to verify your history of diverse credit exposure. A healthy credit report and high credit score both emerge from having a variety of credit available to you. Having a variety of credit options is helpful for an individual’s credit report and helps them keep a high credit score. For a well-balanced credit profile, one should use a credit card and choose both secured and unsecured loans.

A person should avoid applying for several loans at once because this shows lenders that they are credit-hungry. When a loan application is submitted, a credit inquiry will always be made. Applying for loans frequently conveys an unfavourable impression of the applicant to lending organisations, increasing the likelihood that the loan will be denied. Therefore, one should only apply for new credit when they actually need it.

It’s never a good idea to close an individual’s old accounts or credit cards because doing so reveals their lengthy relationship with the financial institution and their extensive repayment history with it. Their previous history with the bank is erased when they close old credit cards or accounts, which has a negative effect on their credit score.

Most credit card companies let customers pay the minimum amount due, which is often between 5% and 10% of the balance owed. A person can prevent a late payment or default in this manner. In addition to interest, the remaining balance is carried over to the subsequent billing cycle. In the long run, he should aim to pay the full amount owing on the account rather than just the minimum amount required in order to prevent accruing interest. One should always make on-time, full payments to keep a decent credit score.

Getting loans approved under their own names might be challenging for people who have no credit history. Even if they are approved for a loan, the interest rates will still be greater than those provided to those with credit histories. In order to keep your credit history and raise your credit score to 750 and eventually close to 900, it may be a good idea to obtain at least one credit line, such as a credit card.

The majority of lenders accept scores that are higher than 750. Before submitting an application for a loan or credit card, these methods should be carefully reviewed in order to obtain lending products at lower interest rates. One may notice a gradual improvement in his or her credit score if these easy steps are taken.

A high CIBIL score is essential and offers several benefits. So, before asking for a loan, a potential borrower needs to be aware of the advantages. Listed below are some of the main advantages of having a high credit score:

This is a significant advantage of having a high credit score. Everyone wants to keep their credit in excellent standing so they can take out loans at reasonable interest rates. This can also speed up loan repayment and significantly lessen the financial load. In the long term, you can save a ton of money by slightly reducing large loans like home loans and loans secured by a property.

Any lender who receives a loan application will check a borrower’s credit history. A person with a high credit score is very likely to get a loan approved because of their strong credit history and a history of making regular and on-time loan payments. A high CIBIL score also indicates that a person hasn’t taken out numerous loans from various lenders or racked up a lot of debt, which makes it challenging to repay the loan. Based of this, the lender is certain that they would repay the loan in full and on time, increasing the likelihood of acceptance to a point where it is almost guaranteed.

A person with a high CIBIL score is likely to be a trustworthy and accountable borrower. As a result, the lender might be more willing to grant them a higher loan amount or a higher credit limit on their card.

In conclusion, maintaining a good CIBIL score requires responsible credit behaviour, such as timely payments, responsible credit utilisation, and a healthy credit mix. Regularly monitoring one’s credit report and taking corrective action when necessary is also crucial for maintaining a good score.

A good CIBIL score can open up a world of financial opportunities and help individuals achieve their goals. Whether one wants to purchase a home, start a business, or finance a major purchase, having a good credit score is essential. By following the tips outlined above, individuals can ensure that they maintain a good CIBIL score and achieve financial success. It is important to note that good financial habits and responsible credit behaviour are key to building and maintaining a healthy credit profile.c

It is also important to keep in mind that a poor CIBIL score can have significant negative consequences, such as being denied credit, paying higher interest rates on loans, and being subject to more stringent credit terms. In some cases, a poor credit score can even limit an individual’s ability to rent an apartment, get a job, or obtain insurance. Therefore, it is essential to take steps to maintain a good CIBIL score and avoid any adverse financial impacts. By staying informed about one’s credit profile and taking proactive steps to improve it, individuals can position themselves for financial success and achieve their long-term financial goals.

CIBIL, or Credit Information Bureau (India) Limited, is India’s first credit information company, which was established in 2000. CIBIL collects and maintains credit records of individuals and companies, which include details such as credit card bills, loan repayments, and credit inquiries. These records are used by banks, financial institutions, and other lenders to assess an individual’s creditworthiness when they apply for loans or credit cards.

A credit score of 750 or above is considered a good credit score, as it reflects a strong credit history and responsible credit management.

To improve your CIBIL score, focus on paying your bills on time, keeping your credit utilisation ratio low, maintaining a good credit mix, and regularly checking your credit report for errors or discrepancies. These actions can demonstrate responsible credit behaviour and help boost your credit score over time.

Visit www.cibil.com to request your CIBIL report. You must first submit your name, PAN card number, date of birth, gender, and other personal information, go through the personal verification process, and pay the fee to view your credit report.

Credit score below 650 is generally considered a bad credit score in India. A low credit score indicates that the borrower is a high-risk borrower and may have difficulty obtaining credit from lenders.

A credit score report summarises an individual’s credit history and creditworthiness. It includes personal information, credit accounts, payment history, and public records. The report also includes a credit score, which is a numerical representation of an individual’s creditworthiness.

No, seeking your own credit score or report will be regarded as a soft check that has no impact on your credit score.

Lenders will send CIBIL all of your financial data every 30 to 45 days. This will contain your payments, any unpaid amounts, any late payments, and more. A smaller lender from whom you have taken out a loan might share your information once every three months.